The Bitter Truth About Moving Insurance in India

Tanuj

Founder, ShiftCompare Technologies Pvt. Ltd. · 2026-03-28

Transit insurance for packers and movers is useful only when you get a real policy document, declared value, item list, and claim process in writing. Basic carrier liability is not the same thing. Before loading, ask who the insurer is, what is excluded, how self-packed boxes are treated, and how quickly damage must be reported.

You may feel stuck. But legally, the moving company might be completely in the right. This problem happens to thousands of families every year because they do not understand the difference between basic carrier liability and actual declared-value transit insurance.

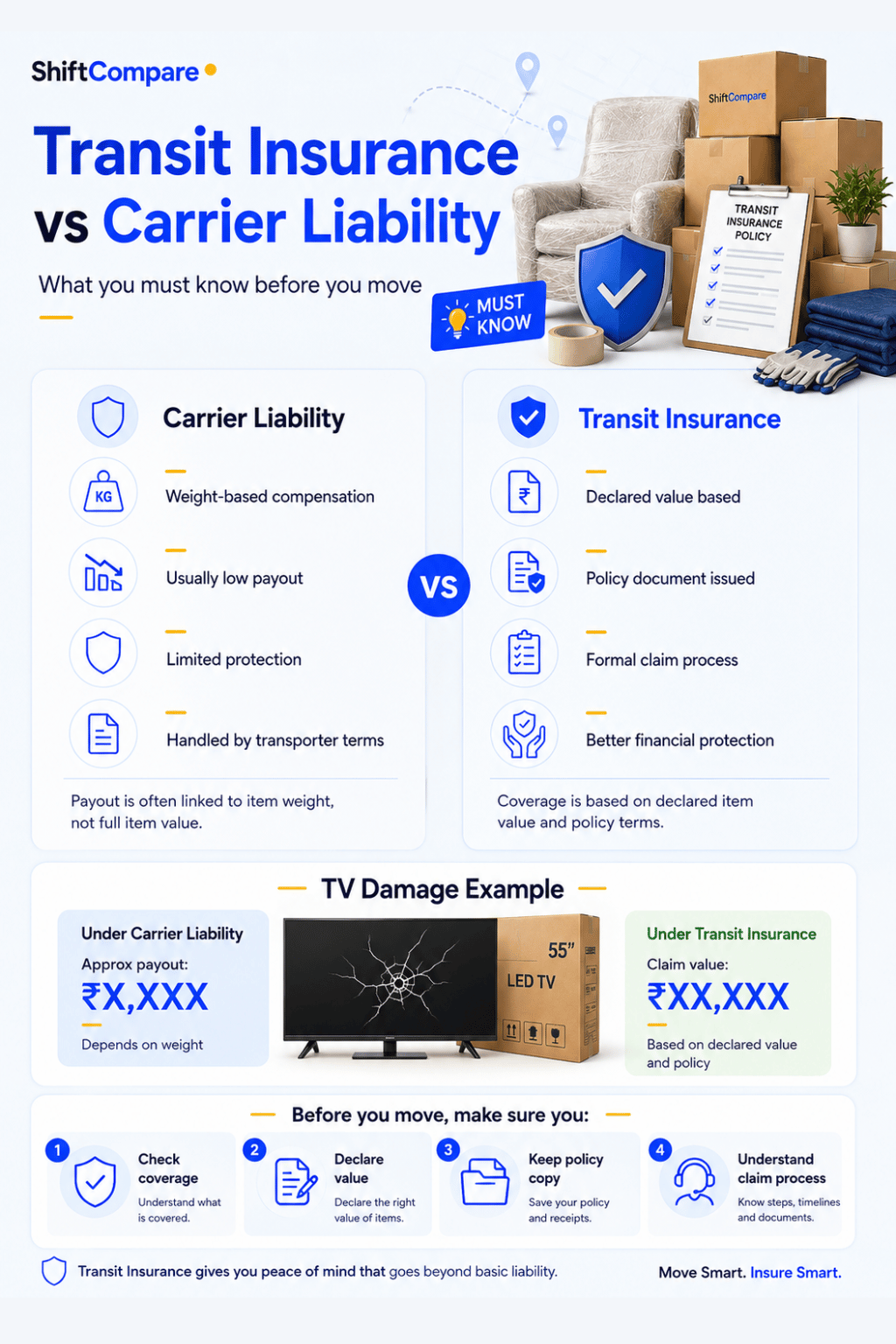

What is the difference between carrier liability and transit insurance?

When a moving salesperson tells you that your goods are insured “by default,” they are talking about Carrier Liability. By Indian law, transport companies have a basic liability for the goods they carry. However, this liability is based on weight, not the monetary value of the item.

The standard carrier liability rate is roughly ₹50 per kilogram. Back to the broken TV: if it weighs 15 kg, you get ₹750. The fact that it was a premium OLED screen does not matter. They pay based on scrap weight.

Declared-Value Transit Insurance is a proper policy covering the actual declared value of your goods. Movers charge a premium of 1% to 3% of your total declared value. For that same ₹80,000 television, a 2% policy costs ₹1,600 in premium. But it covers the full ₹80,000 replacement value.

The math is obvious. Always buy declared-value transit insurance.

What does packers and movers transit insurance cover?

Even with a 3% declared-value policy, read the fine print. Standard full-value coverage includes:

- Road accidents and truck overturning

- Fires during transit

- Severe mishandling during loading and unloading

- Physical damage clearly visible on delivery

It does not cover:

- Internal mechanical faults (washing machine that “won’t start” with no external damage)

- Items self-packed by the customer

- Cash, jewelry, documents, precious metals

- Pre-existing damage that was not documented before loading

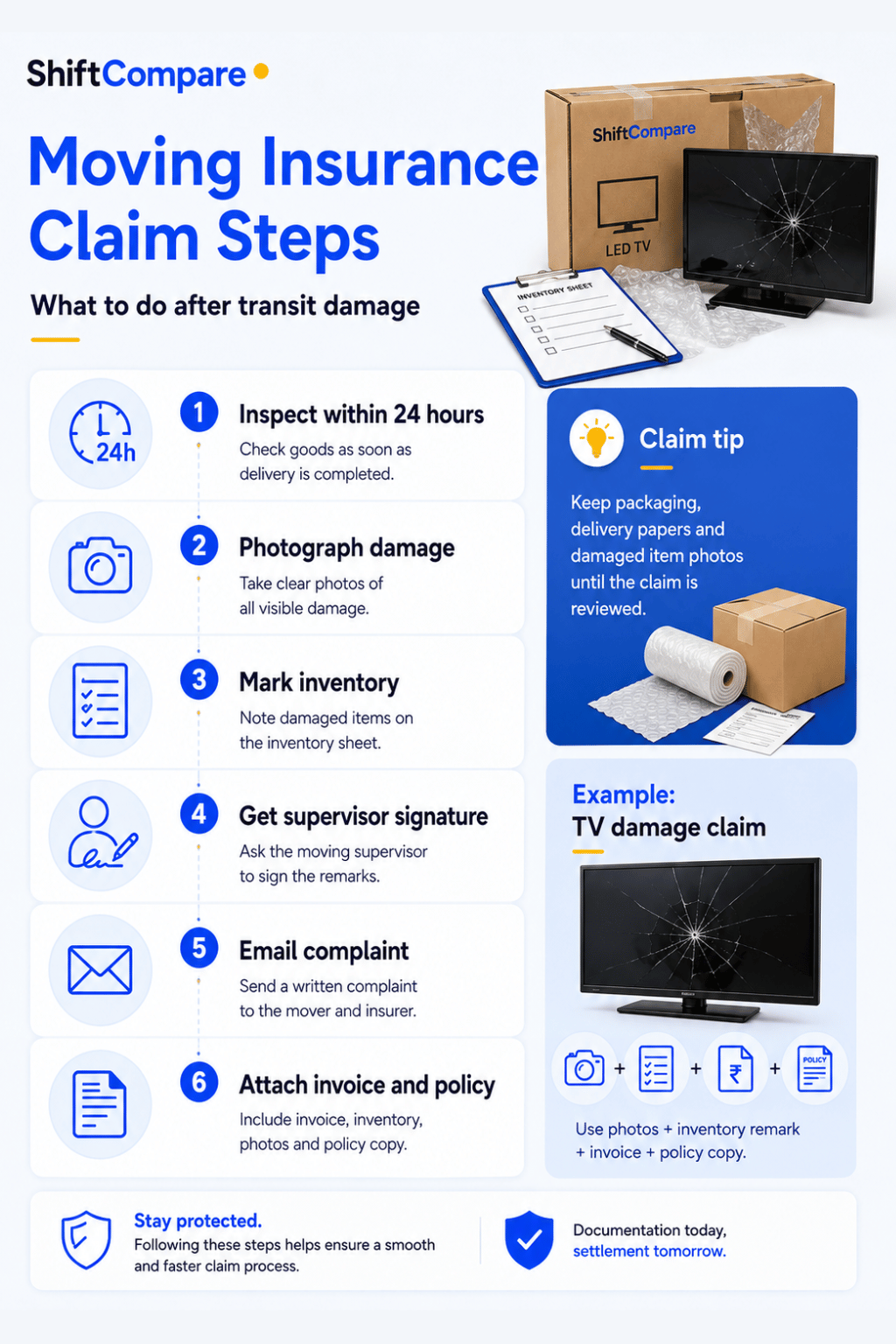

How should you file a moving insurance claim?

If something breaks, act within 24 hours. Waiting three days and then discovering broken plates will get your claim denied. The insurer’s position: you broke them while unpacking.

Step 1: Document the damage within 24 hours of delivery with photographs from multiple angles.

Step 2: Force the delivery supervisor to acknowledge the damage in writing before the truck leaves. Get the inventory list, write the damage next to the specific item description, and get a supervisor signature.

Step 3: File a formal written complaint with the moving company via email with photos, signed inventory sheet, and original invoice attached.

A company handling this process well should assign a claims officer within 48 hours and resolve the claim within two weeks. If they delay beyond 30 days without explanation, escalate to the insurance company directly.

Which official checks help during an insurance dispute?

Ask the mover for the insurer name, policy number, and declared-value schedule. Verify the mover’s GSTIN through the GST taxpayer search guide. If the mover refuses to support a valid claim, keep invoice, policy, inventory, and photos ready for the National Consumer Helpline.

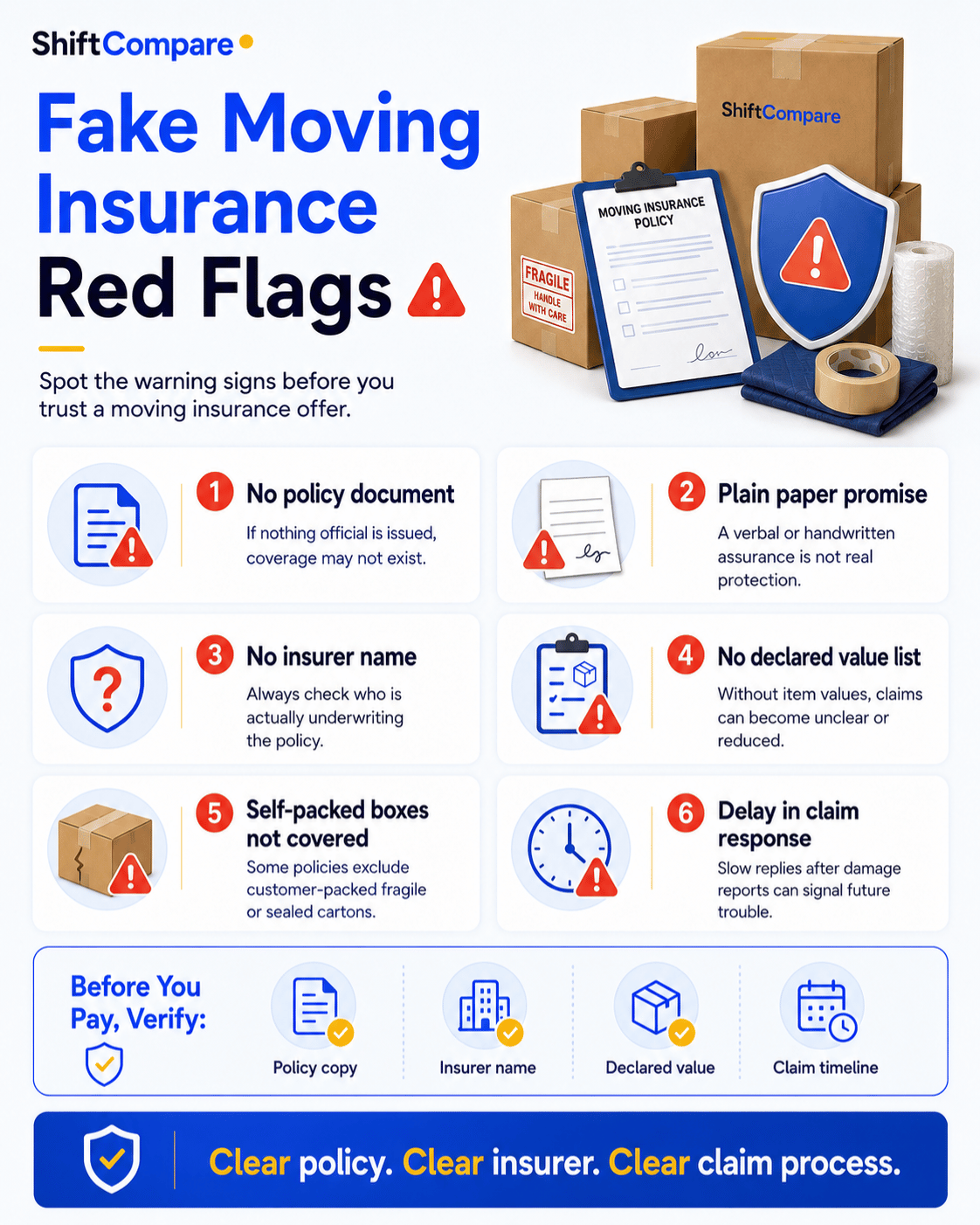

How can you spot a fake moving insurance offer?

Never accept an insurance policy written on plain paper. You must receive a formal insurance certificate from a recognized insurer - HDFC Ergo, ICICI Lombard, Tata AIG, or similar. If the moving company says they handle insurance “internally,” leave. That is a major warning sign.

IBA-approved (Insurance Brokers Association) transport vendors undergo strict financial checks. Corporate HR managers moving employees often mandate IBA-approved vendors specifically to avoid fraud. You can verify a mover’s GST status and business legitimacy using our Verify Packers Movers tool.

For full coverage of moving fraud tactics used in Delhi NCR, read our moving scams guide. If you are managing a high-value move into a premium sector like Sector 67 or DLF Phase 3, declared-value insurance at 2-3% is not optional. For car transport specifically, our car transport guide covers vehicle-specific insurance requirements. Whether you’re doing a local Gurgaon shift or a 2,000 km intercity move, use our moving calculator to factor the insurance premium into your total budget.

Insurance advice is different from insurance pricing

A premium table tells you what insurance may cost. A claim discussion tells you whether the cover will help when something breaks. Keep those two questions separate. For premium ranges and bill lines, use transit insurance charges for packers and movers. Here I am focusing on the human question: should you take it, what should be written, and what proof should you keep?

I have seen families pay for insurance and still get stuck because the declared value was vague. “Household goods covered” is not enough. Covered for how much? Against what risk? With what exclusions? Under whose name? These details matter more than the sales pitch.

| Insurance detail | Weak wording | Better wording |

|---|---|---|

| Declared value | Goods insured | Goods insured for Rs 2,50,000 declared value |

| Policy proof | Insurance included | Policy copy or written insurer details before dispatch |

| Claim timing | We will handle | Claim process and required photos explained |

| Damage scope | All damage covered | Transit accident, fire, theft, rain, handling terms listed |

| Invoice link | Cash insurance | Insurance amount shown on quote or invoice |

When I strongly suggest insurance

For local small moves, insurance may not always be essential. If you are moving a few cartons and a basic bed within the same neighbourhood, careful packing and a good crew may be enough. But for intercity moves, expensive electronics, glass tables, imported furniture, bikes, cars, or storage-linked moves, I strongly suggest insurance.

Long routes like Delhi to Bangalore, Gurgaon to Pune, and Noida to Pune add more time, more road risk, and sometimes more handling. That is exactly where insurance should be discussed before booking, not after the truck leaves.

Photos are part of insurance, not an extra habit

Take photos before packing, after packing, during loading, and at delivery. Take close shots of TV screens, fridge doors, washing machine panels, glass tops, and bike or car panels. If there is a claim later, photos cut through arguments.

Also keep the inventory list. If your 55-inch TV is not listed anywhere, claiming damage becomes harder. The mover may say it was not part of the consignment. Sounds silly, but disputes often become silly because proof is missing.

What fake insurance usually looks like

Fake insurance is usually sold with confidence and no paperwork. The mover says, “Sir, 3 percent insurance, full safe.” You pay. No policy comes. After damage, they say insurance company is delaying it. Then they stop answering.

Before loading, ask for the insurer name, policy type, declared value, and claim process. If they cannot share everything immediately, at least get the exact insurance terms written into the quote. If the quote is otherwise unclear too, read moving scams in Delhi NCR before you continue.

Insurance for cars, bikes, and high-value items

Car and bike transport need extra discipline. A vehicle has visible panels, odometer reading, fuel level, documents, and accessories. For cars, read Delhi to Bangalore car transport and car transport charges in Gurgaon. For bikes, compare bike transport charges. Take a handover checklist seriously.

For household goods, expensive items should be named separately. A piano, aquarium, gaming PC, marble table, or large artwork should not hide inside “miscellaneous.” If the item is valuable enough to worry about, it is valuable enough to list.

My insurance rule before dispatch

Do not buy insurance because the mover says it is standard. Buy it because the route, item value, and handling risk justify it. Then make the paperwork match the promise. Insurance without declared value, proof, and claim steps is not peace of mind. It is just another line on the bill.

Claim readiness before loading

Before loading, keep three things ready: inventory, photos, and declared value. The declared value should be believable. Do not declare Rs 10 lakh for goods that are worth Rs 2 lakh, and do not under-declare expensive electronics just to reduce premium. Either mistake can hurt later.

At delivery, inspect high-value items before signing a clean receipt. If the crew is rushing, slow down politely. A delivery sheet with damage noted is much stronger than a phone complaint the next day.

Insurance is not magic. It is paperwork plus proof. The better your proof, the better your chance of a fair claim.

My honest view: take insurance when the route or item value justifies it, and then behave like a claim may happen. That mindset protects you.

When insurance is not enough

Insurance cannot fix bad packing, poor loading, or missing inventory. It only helps after a covered loss. So do not use insurance as an excuse to accept careless handling. A good move needs both prevention and paperwork.

If the mover packs fragile goods badly and then says insurance will handle it, stop and correct the packing. Claims take time. Prevention is faster.

Also remember exclusions. Some policies may not cover self-packed cartons, pre-existing scratches, cash, jewellery, documents, plants, or liquids. Keep those items with you or list them separately if the mover accepts responsibility.

Insurance is a safety net, not the main plan. The main plan is good packing, careful loading, clean inventory, and honest documentation.

How to discuss insurance without panic

Do not let insurance become a fear sale. Ask calmly: what is covered, what is excluded, what value is declared, what proof will I receive, and how do I file a claim? These five answers are enough for most moves.

If the mover answers clearly, good. If the mover says everything is covered but cannot explain the document, slow down. Insurance should reduce uncertainty, not add another vague promise.

For expensive goods, write item names separately. For regular cartons, keep the inventory clean. That balance is practical and fair.

A fair way to choose declared value

Declared value should be close to real replacement value, not emotion and not guesswork. Make a quick list of expensive items: TV, fridge, washing machine, laptop, desktop, sofa, dining table, bike, or artwork. Add a practical value beside each. Then use that to discuss insurance.

If the mover suggests a very low declared value to reduce premium, ask what happens if the actual loss is higher. If they suggest an inflated value without proof, ask whether the insurer will accept it. Both extremes can create trouble.

For most families, a clear declared-value list is enough. It shows that you thought about the risk before loading, not after damage.

Tanuj

Founder, ShiftCompare Technologies Pvt. Ltd.

Tanuj runs ShiftCompare.in and CratoShift.in, having helped 500+ Delhi NCR families compare movers and avoid overcharging. He writes from actual field experience, not press releases.

LinkedInFrequently Asked Questions

Will transit insurance cover my jewelry and cash?

No. Transit insurance policies specifically exclude cash, jewelry, important legal documents, and precious metals. You must carry these high-value, small items with you personally in your own car or flight bag. Moving companies will refuse to load them onto the truck.

Can I buy transit insurance if I pack the boxes myself?

Generally, no. Insurance companies only provide full declared-value coverage for items packed by the professional moving crew. If you pack a box yourself, the insurer cannot verify the condition of the items before transit, so they classify self-packed boxes as completely uninsured.